All Categories

Featured

Table of Contents

You'll fill up out an application that has basic personal info such as your name, age, etc as well as a more in-depth questionnaire about your medical history.

The brief response is no., for example, allow you have the comfort of death benefits and can build up cash money value over time, indicating you'll have more control over your benefits while you're active.

Cyclists are optional arrangements included to your plan that can provide you additional advantages and defenses. Anything can take place over the program of your life insurance policy term, and you desire to be ready for anything.

There are circumstances where these advantages are constructed right into your policy, yet they can also be offered as a separate enhancement that calls for added payment.

Top Term Vs Universal Life Insurance

1Term life insurance policy uses momentary protection for an important period of time and is generally less costly than irreversible life insurance. 2Term conversion standards and constraints, such as timing, may use; for example, there might be a ten-year conversion privilege for some products and a five-year conversion opportunity for others.

3Rider Insured's Paid-Up Insurance Purchase Choice in New York City. 4Not readily available in every state. There is an expense to exercise this cyclist. Products and riders are offered in approved jurisdictions and names and features might vary. 5Dividends are not guaranteed. Not all participating plan proprietors are qualified for returns. For pick cyclists, the problem relates to the insured.

(EST).2. On the internet applications for the are offered on the on the AMBA site; click the "Apply Now" blue box on the right-hand man side of the web page. NYSUT members can also print out an application if they would certainly favor by clicking the on the AMBA internet site; you will then require to click on "Application" under "Kinds" on the right-hand man side of the web page.

Term 100 Life Insurance

NYSUT participants enlisted in our Degree Term Life Insurance Policy Strategy have actually access to offered at no added price. The NYSUT Member Advantages Trust-endorsed Degree Term Life Insurance policy Strategy is underwritten by Metropolitan Life insurance policy Firm and provided by Organization Member Advantages Advisors. NYSUT Trainee Members are not qualified to take part in this program.

Term life coverage can last for a set period of time and typically has preliminary rates that raise at established intervals. Normally, it does not construct cash money value. Permanent life coverage, likewise recognized as whole life insurance coverage, can last your entire life and might have higher preliminary rates that do not usually enhance as you get older.

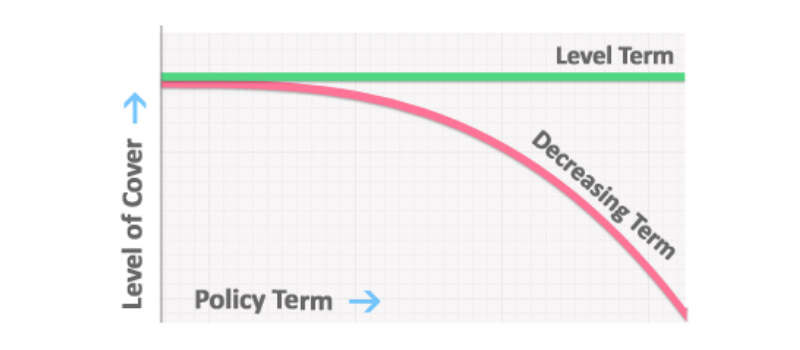

Our term life options include 10, 15, 20, 25, 30, 35, and 40-year policies. The most prominent kind is level term, implying your payment (premium) and payment (survivor benefit) remains level, or the same, till completion of the term duration. This is one of the most uncomplicated of life insurance policy choices and requires really little upkeep for plan proprietors.

As an example, you might provide 50% to your spouse and divided the rest among your grown-up children, a moms and dad, a good friend, and even a charity. * In some circumstances the survivor benefit might not be tax-free, find out when life insurance is taxed.

This is despite whether the insured person dies on the day the policy starts or the day prior to the policy ends. Simply put, the amount of cover is 'degree'. Legal & General Life Insurance Policy is an instance of a level term life insurance policy plan. A degree term life insurance policy plan can match a large variety of scenarios and requirements.

Your life insurance policy policy might also form part of your estate, so can be based on Estate tax learnt more concerning life insurance policy and tax. what is direct term life insurance. Let's take a look at some features of Life Insurance from Legal & General: Minimum age 18 Maximum age 77 (Life insurance policy), or 67 (with Critical Health Problem Cover)

Tailored Decreasing Term Life Insurance

The quantity you pay stays the exact same, but the degree of cover reduces approximately in line with the way a repayment mortgage lowers. Reducing life insurance coverage can aid your enjoyed ones stay in the family home and stay clear of any type of further interruption if you were to pass away.

Life insurance coverage is a crucial method to secure your loved ones. Level term life insurance policy is what's recognized as a level costs term life insurance coverage policy.

A level term life insurance plan can give you comfort that the people who depend on you will have a fatality advantage throughout the years that you are intending to support them. It's a way to aid care for them in the future, today. A degree term life insurance policy (often called level premium term life insurance policy) plan provides insurance coverage for a set variety of years (e.g., 10 or two decades) while keeping the premium repayments the same throughout of the plan.

With level term insurance, the cost of the insurance policy will remain the very same (or possibly decrease if rewards are paid) over the regard to your plan, generally 10 or two decades. Unlike long-term life insurance, which never ever runs out as lengthy as you pay costs, a degree term life insurance coverage policy will finish at some time in the future, usually at the end of the period of your level term.

Innovative Decreasing Term Life Insurance Is Often Used To

Due to the fact that of this, many individuals use long-term insurance as a steady financial preparation tool that can serve several demands. You may be able to convert some, or all, of your term insurance during a set duration, normally the very first ten years of your plan, without needing to re-qualify for protection even if your health has actually transformed.

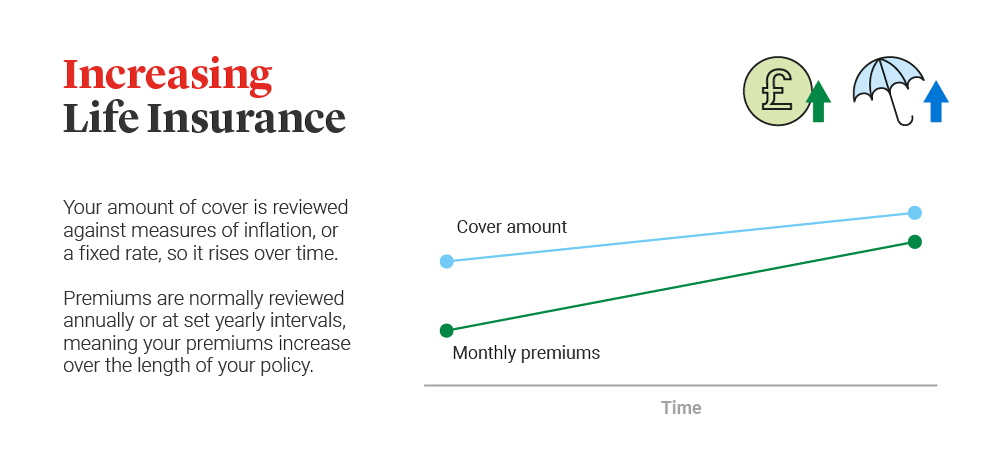

As it does, you may want to add to your insurance protection in the future. As this occurs, you may want to eventually minimize your fatality benefit or think about converting your term insurance coverage to a long-term plan.

{kind=link}

Latest Posts

Final Expense Over The Phone

Funeral Insurance Us

Life Insurance Policy To Pay For Funeral